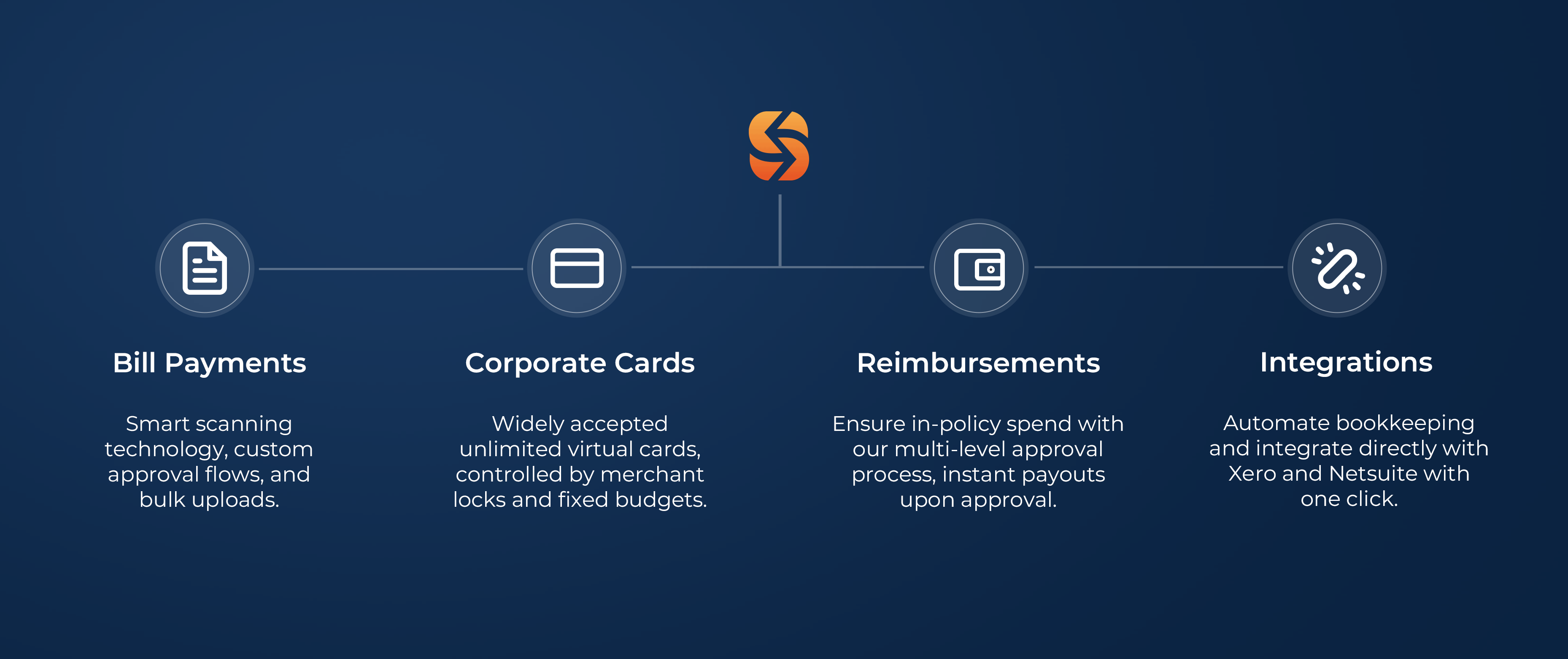

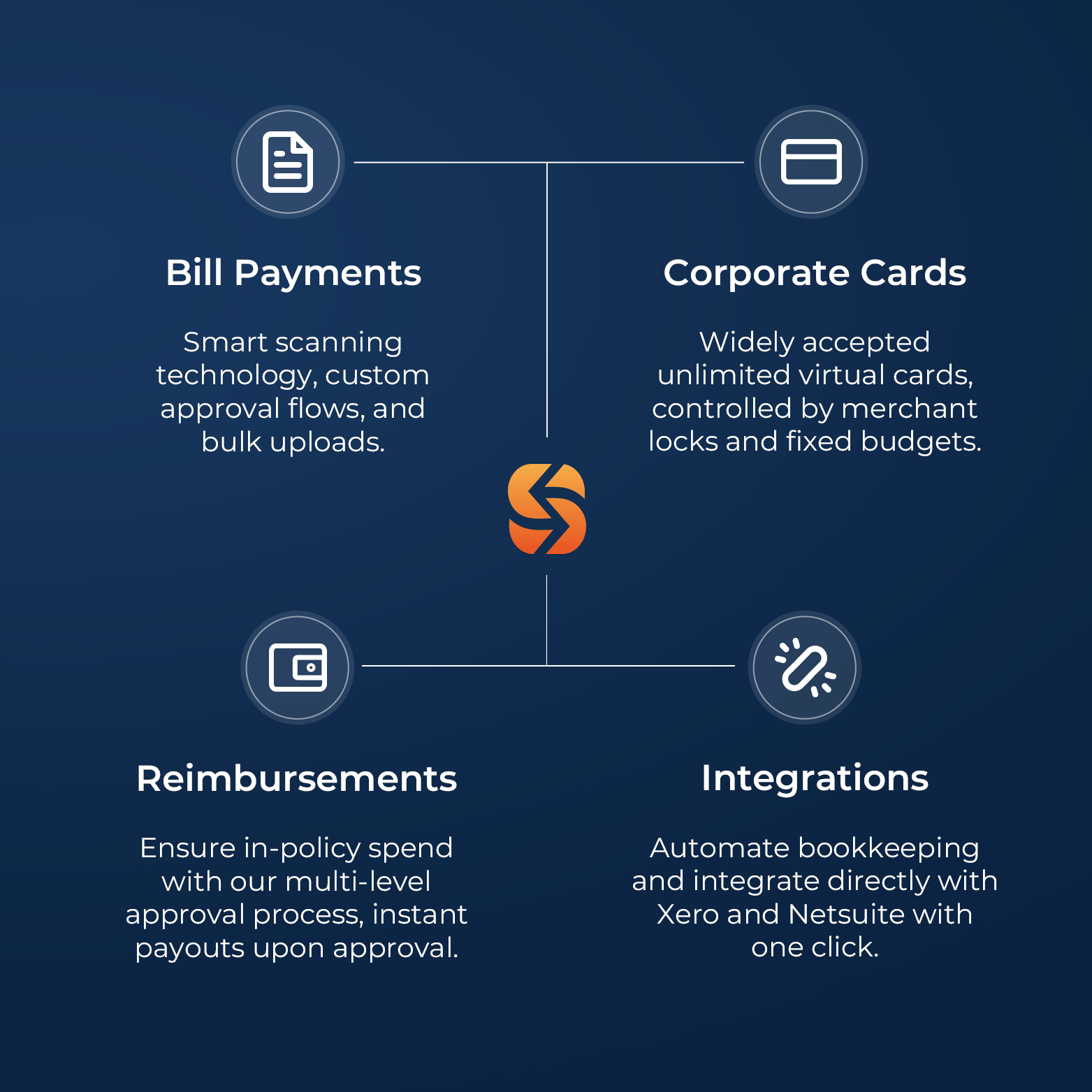

Efficiency and Cost-Saving

Smart automation with guardrails, drive productivity and uncover cost savings

Gain Flexibility and Control

Seamless claims processing with spend and budget controls

Eliminate Out-of-Policy Spend

Enhance visibility with real-time dashboard and customisable approval flow

Reduce Reconciliation Headaches

Seamless accounting integration reduces manual entry and errors

-4.gif?width=991&height=731&name=reimbursements%20gif%20(1)-4.gif "Upload Invoice, fill up the form, and instant settlement upon approval using Spenmo")

ISO 27001 Certified

Spenmo's ISO 27001 certification signifies rigorous adherence to global information security standards, assuring clients that their data is meticulously safeguarded against potential threats.